Set the Market Free

- You can’t rate-hike oil/gas supply and demand back into equilibrium because no matter the rate, the SUPPLY is artificially constrained! We’ve never tried this before in a managed economy, only in a free market economy, which we no longer have due to artificial government intervention in the free market for petroleum. Good luck to us!

Background. Fiscal Policy consists of Congress exercising budgetary control to spend or reduce spending from various departments (such as Defense or Health). Funding is the responsibility of Congress, and Congress states its preference for policies by increasing their funding and contrary sentiment via funding reductions. “Backdoor” ways the President influences policy is through un/favorable – overregulation or by cutting regulations, or Executive Order, which can carry the weight of a law or nearly so, just by his or her unilaterally signing a piece of paper. In the present case, the President and cohorts have cut the fully-utilized supply of petroleum by about 12%.

Inflation Mandate. Let’s start with the time-honored expectation that the nation’s institutions smite inflation with the mace of higher interest rates; the Fed wields the handle. This could be; it has been shown to be so several times; it inductively rings true. This approach works over the markets and economy by strangling productive activity… sledgehammering it time and again on the larynx with interest rate hikes until the economy chokes “Uncle…” (unable to cry out “Uncle”), rolls over into recession, and demand capitulates.

In a free market economy, what happens when demand is choked off is that the bottom drops out from price supports and inflation’s upward spiral stalls, loses momentum, flattens, and starts to descend until the interests of wanters resuscitate consumption. Whether this involves a recession depends on a number of factors – controllable, uncontrollable, and unknown.

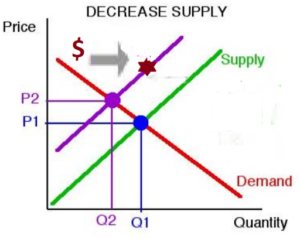

The Law of Supply and Demand. So the intersection of the eternal “X” comprising supply and demand is reestablished in a different cartesian coordinate on the Cartesian map, having been severely distorted by the above Executive Orders. But what happens when that upsloped Supply Curve is artificially shifted vertically, dramatically, inexorably, inflexibly, ignorantly? The price point is driven higher than the equilibrium while demand does not respond to price, adhering to other economic factors. For example, in gasoline, demand would now be supported by the humanistic and economic need to move people and things.  There is some minimum that, regardless of price, will mark a bottom minimum of quantity and price, but this is not an equilibrium; it is forced. Think about military gas, plus emergency use gas, plus politicians’ gas. At least the essentials sold at the never-lower-than price, which at this stage in the model lies above the equilibrium point because it’s been shoved upward like a barbell lifted by Milo. In the end something’s gotta give and that’s quality of life. People used to having will have not, either due to supply restrictions or price. The supply side, where we started, will float there or higher, soaking up all the money possible from each commodity until it’s no longer possible to make tradeoff decisions; price floats ever higher, and if there are imports, those suppliers will enjoy premium prices; supply continuity breaks down.. We end up with business, personal, production, and consumption demands all chasing the next necessary product, with business production supply unable to sustain economic production quotas nor balance cross-industry input streams for efficiencies.

There is some minimum that, regardless of price, will mark a bottom minimum of quantity and price, but this is not an equilibrium; it is forced. Think about military gas, plus emergency use gas, plus politicians’ gas. At least the essentials sold at the never-lower-than price, which at this stage in the model lies above the equilibrium point because it’s been shoved upward like a barbell lifted by Milo. In the end something’s gotta give and that’s quality of life. People used to having will have not, either due to supply restrictions or price. The supply side, where we started, will float there or higher, soaking up all the money possible from each commodity until it’s no longer possible to make tradeoff decisions; price floats ever higher, and if there are imports, those suppliers will enjoy premium prices; supply continuity breaks down.. We end up with business, personal, production, and consumption demands all chasing the next necessary product, with business production supply unable to sustain economic production quotas nor balance cross-industry input streams for efficiencies.

What has happened in this situation is that price escalation has been guaranteed regardless of demand, and attendant demand is artificially maintained by the government for essential public needs. Oligarchies of various items ensue, enjoying price protections and supply protections, which now must be managed by the government. This economic situation is back door Communism, not of the Soviet iron-fist sort, but of the Marxian economic sort.

Double Whammy. What the external consumer, and by that I also include the business as consumer of goods in raw as well as intermediate role, sees is tenacious inflation. This can occur in commodities, simply constructed goods like tampons and aluminum cans (and their components such as pulp, resin, metals, suspension powders, and the like), complex construction products like tractors, and entire complexes like office parks and semiconductor chip plants. In other words, such price fixing or “price meddling” via governmental edict can be pervasive if the supplier network for key BOM items is affected by non-market forces. Therefore, the product managers of all the parts and suppliers in the supply chain are not in control of what is created, what quantity, its location, or its next destination. Some or all of these factors are determined by the skewed effect of the Governmental Policy on Price – which affects item pricing all through the BOM – and also effected by external forces such as the Emergency Mandate such as the Defense Producttion Act – which affects item utilization and its supply.

On top of Fiscal Policy twisting supply and demand balance, a series of cash injections, warranted and unwarranted, floods the economy with unearned liquidity while the Fed pumps even more money into the economy by creating and buying $trillions in government notes. The US Federal government unleashes about $7 trillion on the economy. Some of this is due to anticipation that shutdowns will cripple the economy to the extent it cannot supply food and utilities to the population. Of course, that did not happen, but possibly partly due to the cash injections. Too much cash flowing to consumers made their buying choices far easier and less subject to individual scrutiny. Prices surged with the last 30% dumped into an already recovered economy.

Monetary Policy. Closing out our discussion of policy interference in Supply and Demand Laws, we will now turn to Monetary Policy and its effects in price establishment and inflation, and its relation to the supply and demand control/interference of government intervention in natural market forces, just to contrast Fiscal Policy with Monetary Policy:

Because Monetary Policy consists of only two parts, the ways that any change can be effectuated are limited. The Federal Reserve, US’s national banking system, performs both aspects of Monetary Policy; they are flooring interest rates and managing purchased US notes. The Fed, as it’s known, in its 11 regional branches, facilitates the flow of money through the economy. By raising floor interest rates, it forces commercial banks to increase their rates to a higher level in order to make a profit on lending instruments. This in turn forces businesses to raise their bond rates even high than that. Raised rates have the effect of reducing economic activity, and can be used to “cool off” an economy where rampant price increases are causing inflation. The Fed can also buy US issued bonds to finance more spending by the US government, which increases economic activity by increasing the money supply for federal procurement. The opposite, selling those bonds, has a de-stimulaing effect and tends to cool off inflationary price increases.

As inflation occurs, it should be possible to moderate it or reverse it both by throttling down on asset (bond) issuance and by increasing the cost of borrowing money by bumping up rates. It’s the Fed’s charter to keep inflation at or below 2%. Any peek above that level should be responded to by a rate hike, and even below that level, a trending rise in prices can be attenuated by applying a small rate hike of .25%. The rates cannot be continuously fiddled with though; also the Fed is usually reluctant to do so because the reaction to a rate hike is swift and dramatic in business outlooks and the stock market usually has a short term negative response. The stock market looks ahead and sees that higher rates will make business spending more expensive and in the future curtail investments in hard assets (equipment for example) and research and development. But anyhow, based on sophisticated judgment, rate changes have to be done.

Fiscal Policy Transcends Monetary Policy. This is where the push-pull of Fiscal Policy and Monetary Policy collide however. Monetary policy can reduce the irrational push up of prices based on business desire to earn more and labor’s desire to increase wages. But Monetary Policy cannot overcome price hikes outside the normal range of Supply and Demand equilibrium. When Fiscal Policy pushes the Supply Curve leftward artificially, prices go up dramatically. This is not the result of normal Supply/Demand balancing as is found in free markets. It is a “bastardization” of one part of the economic model that raises prices without underlying supply increases. That means businesses affected will automatically see a bump in revenues without having to support them with increasing supply, which means unitary costs become lower and the businesses are more profitable. What consumers see, and by consumers I also mean businesses that are procuring items, is a raise in prices without corresponding benefits, which to retail consumers would mean more purchasing power and for business consumers would mean increased production capability. All that happens in this regard is that prices escalate.

Low Unemployment Sparks Wage Price Spiral. Another bogeyman hidden in the woodpile is the labor base. Now, another charter of the Fed is full employment. Usually that would mean something in the 4.5% range give or take, or about 95.5% of employable persons have a job. When employment gets much higher, businesses must compete harder for employees and do that by increasing overall wages and benefits. When the unemployment rate is very low, open positions increase, employers needing labor raise job offer amounts to hire and also raise existing salaries to retain employees. Let’s take a quick step aside and discuss currently-hidden unemployment, which is able-bodied adults below retirement age (18 to 67 year old) who are not seeking employment because they can subsist on government dole. This is a tremendous drag on the economy, being in the neighborhood of seven million persons who could be filling the equivalent number of open jobs, When this is happening and price levels are increasing due to artificially short supply, people have a tendency to reduce savings because their dollarized earnings are decreasing; prices and wages both go up. This is called a wage/price spiral and is very very hard to overcome. In fact, if you think about it, Monetary Policy alone cannot solve this problem because the Fiscal Policy that underlies it is not affected by the Monetary actions taken by the Fed. If the Fed continues its futile attempt to affect pricing, it will drive rates up so high that monetary fluidity will diminish to a choke point state and a dramatic reduction in business activity will occur… a recession. We will have inflation and recession occurring at the same time. If prices rise due to government Fiscal Policy, no amount of Monetary Policy can bring prices back into line. This is the worst scenario of all: Stagflation.

Government Subsidizing Consumers Makes It Worse. To exacerbate the above, if unemployment benefits are high enough to hold workers out of the workplace, the wage portion of the wage price spiral increases very quickly with attempts to motivate voters by increasing the minimum wage. Still, people remain on the unemployment sideline, and the transfer payments that supply them with subsistence living do not improve the national productivity, and GDP suffers. The less the body of able workers in the US produce individually, the lower the national productivity will be. It’s just the sum of the work we all do and what we do with out lives to build rather than just absorb benefits. This is another factor dragging down the economy. Business are faced with higher rates, capped quantities of goods to procure, increased prices for those goods, inability to hire, plus higher wages for those available to hire or hold in jobs, .

Conclusion. So we have seen how the mere artificial disruption of supply/demand balances of one or more key commodities can throw off the entire basis of the economy, when applied to essential goods or services – either a commodity or a sector. Hit out at any scarce, core, essential commodity, and an entire economy can be destabilized through all the “four M” factors of production: “Materials,” “Machinery,” “Manpower” (today we call it “People Power”), and “Money.”

This is the bottom line of Fiscal Policy. If our Policy is not one of capitalism and letting the free market determine prices and demand, thus managing the efficacy and efficiency of an operational economy, we will end up with significant distortions between goods and services, and money and consumption. The “unseen hand” that guides us to the greatest use of resources is absent; we see nonessential goods piling up and essential good shortages.

And this is the bottom line of Monetary Policy. Monetary Policy is able to affect pricing considerations only within the parameters set by Fiscal Policy. It is not the spiked cudgel that defeats all inflation, but a tuning tool that can help facilitate smooth economic functioning by increasing or decreasing the velocity of money.

The independent Fed cannot overcome the policies set by the Executive Branch plus the Legislative Branch. If the Legislative Branch lets the Executive Branch create Fiscal Policy, and the Fed is within the Executive Branch, we can see what will befall the economy. It will perform as dictated by the Fiscal Policy accepted by and promoted by the President, who is unlikely to be an economist and responsible manager. The economy will be led by the nose to conduct whatever social policies seem to benefit those of the faction, be it large or small, that leads the President.

Bonus Bottom Line: The Limits of Rates. At one time we had a market-driven economy. What that means is the X equilibrium is allowed to set its own level by adjusting the supply and demand lines based on the quantities produced versus the quantities needed, and the price producers desire to charge versus the amount the buyers will pay. These four factors are driven by the actors in the economy themselves, and the government is not involved in setting them. But at this moment we do not have a market-driven economy for energy, the most important commodity. Supply has been artificially constrained by central mandate to a level far be low demand. When that supply balloon is squeezed, what pops out is price, which goes up dramatically, driving the price of everything that depends on energy higher too. Well, everything depends on energy, so the price of everything is going up. Not only does this affect domestic prices, but since energy production is a worldwide zero-sum gain, reducing the global supply has affected the global price too. It’s like saying the hole is only in one end of the boat; it affects the whole boat anyhow. Beating on this problem with the cudgel of rates is not going to change this situation; it will not unleash more supply. You can’t rate-hike oil and gas back into equilibrium because no matter the rate, the supply is artificially constrained! We’ve never tried this before in a managed economy, only in a free market economy, which we don’t have. Good luck to us!